Equity Retail Brokers is known for its expertise in the Greater Philadelphia banking sector, but the team recently decided to zoom out for a big-picture look at the national data on U.S. bank real estate over the past 20 years.

Using five-year increments running from 2003 to 2022, Equity Retail Brokers’ banking experts dove into the FDIC numbers to produce national-level analyses in four areas:

- New formations of banking institutions

- Business combinations (i.e., mergers and consolidations) in the sector

- Branch office relocations

- Branch office openings and closings

Running the analysis was David Laiter, whose focus as a member of the Investment Sales Team includes marketing bank properties for sale in Pennsylvania and New Jersey.

“We knew the trends well, as did the rest of the industry, but we wanted to see the numeric data,” Laiter explained. “Our findings really emphasized the major changes occurring in the banking industry and the evolution of banks’ real estate needs.”

Big changes in banking-industry real estate

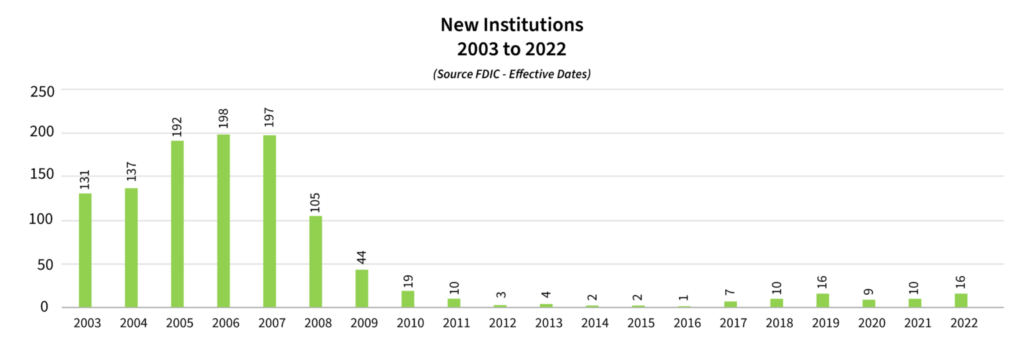

Over time, the decline in newly formed banking institutions (see chart below) was one noteworthy change, observed Principal Ed Ginn, who has been conducting real estate sales and dispositions on behalf of local, regional, and national banks since founding Equity Retail Brokers 27 years ago.

From 2003 to 2007, Ginn noted, the United States saw the introduction of 855 new banking institutions—a remarkable period of growth. “The formation of new banks used to be relatively common,” Ginn said. “In our market alone from ’03 to ’07, we saw the formation of Conestoga Bank, Continental Bank, First Priority Bank, First Resource Bank, Penn Bank, Meridian Bank, The Bank of Princeton, and Liberty Bell Bank.”

Fast-forward to the last period studied—2018 to 2022—and the number of new institutions nationwide had dwindled to just 61. “During this period, there wasn’t one new bank started that was headquartered in Pennsylvania or New Jersey,” Ginn said.

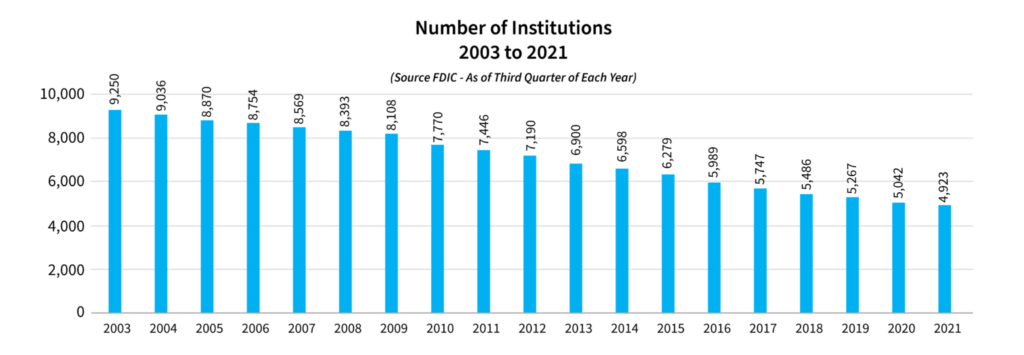

The total number of U.S. banking institutions (see chart below) has been in decline ever since. “In 1992 14,142 banking institutions were reporting to the FDIC,” Ginn said. “Today, there are 4,755. If the trend continues, there will only be 3,814 institutions reporting to the FDIC by 2032.”

The reduction is mainly the result of business combinations. For example, in the Philadelphia Metro Market, WSFS grew by purchasing Bryn Mawr Trust, Beneficial Savings Bank, Continental Bank, and Alliance Bank.

Accelerating bank branch closures

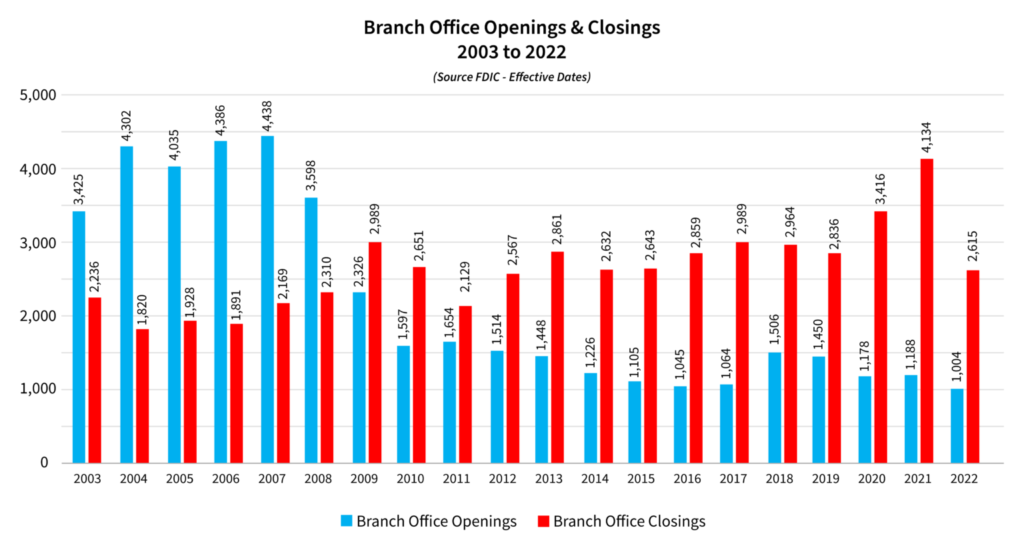

Another big shift, of course, was the acceleration of U.S. bank-branch closures during that two-decade span. Here’s the breakdown of closures per Equity Retail Brokers’ analysis, also portrayed in the chart below:

- 2003 to 2007: 10,044

- 2008 to 2012: 12,646

- 2013 to 2017: 13,984

- 2018 to 2022: 15,965

“All told, we’re talking about 52,639 branch closures across the country,” Laiter said. “That’s compared to 23,013 new branch openings during that same period. The trendline toward a reduced national footprint is quite clear.”

[RELATED: Bank Properties for Sale: Why Handling Bank Transactions Requires Flexibility and Finesse]

A healthy industry

The casual observer might see such statistics as pointing to a decline in the banking sector over time. However, banks have done quite well in the United States and abroad, weathering shocks like the Great Financial Crisis and the Covid-19 pandemic to earn record-setting profits.

“Banks are now gearing up for some tougher times with the possibility of a recession in the second half of the year, but this is still a fundamentally healthy industry,” noted David Goodman, Principal, who has more than 12 years of experience in handling banking sector real estate transactions. “The closures we have seen and continue to see are more about the rise of easy and quick Internet banking and the long-term trend toward consolidation. Simply put, banks just don’t need as much real estate as they once did.”

The role of consolidation in fueling banking real estate dispositions and sale-leasebacks is easy to overlook, Ginn adds.

And the industry has seen a lot of consolidation over the decades.

In October 2018, the financial news outlet Motley Fool published an overview titled, “The Biggest Mergers & Acquisitions in Banking.” According to the author, today’s “Big Four” U.S. banks—Citigroup, Wells Fargo, Chase and Bank of America—“were actually 35 separate companies in 1990.”

When banks consolidate, their real estate does, too. “This inevitably leads to excess branch locations,” Ginn said. “If you look at the stats from the past 20 years or so, for every merger there has been an average of 8.7 bank branch closings.”

[RELATED: Equity Retail Brokers’ Banking and Financial Industry Newsletter]

Opportunities in bank branch real estate

The profitability and shifting competitive dynamics in the U.S. consumer banking sector continue to generate an enormous amount of real estate activity. Goodman points to the branch relocations charted by Equity Retail Brokers in its 20-year analysis.

“You had 23,013 relocations during that period, which translates into strong demand for services that we and other firms provide,” the executive explained. “That includes lease renegotiations, consulting on site-selection strategy, handling bank-branch dispositions and conducting sale-leaseback transactions.”

[RELATED: Sale-Leasebacks for Banks: Tips for Achieving Maximum Results]

Last year, the merger of BB&T Corp. and SunTrust (now Truist) led to a change of signage and colors at 97 BB&T locations in the Delaware and Lehigh Valleys.

When consolidated banks evaluate their rebranding strategy, they often prioritize their highest-visibility locations in the market, along with examining factors such as branch success, total branches and real estate quality.

“In new and existing markets, they may want to get that new branch in front of as many people as possible,” Laiter notes. “That might mean closing a large branch in a lower-traffic area and relocating to a smaller-footprint site where traffic volume is higher.”

In other cases, though, the banking institution might favor locations with superior ingress and egress or higher real estate value. “Many different factors can drive real estate decisions in retail banking,” Laiter said.

And importantly, Ginn adds, banks continue to explore new markets and open new branches across the country. KeyCorp’s KeyBank, for example, jumped into the Philadelphia market back in 2016 after buying First Niagara Financial Corp., reportedly for $4.1 billion. Chase has been pursuing a major expansion over the past couple of years with its plan to open 400 new branches and hire 3,000 employees in 48 states.

“When you look at the branch openings data, there were actually more openings—6,326, to be exact—from 2018 to 2022 than from 2013 to 2017, where you had 5,883 branch openings,” Ginn said. “Bear in mind, too, that the ’18-to-’22 period included the disruptions brought on by Covid. So branch openings are humming along with quite a bit of stability, even though the scale isn’t what it was 20 years ago.”

Equity Retail Brokers has on multiple occasions assisted banks with real estate strategy in the wake of M&A. Goodman points to WSFS Financial Corp.’s $1.5 billion acquisition of Beneficial Bancorp, Inc., in 2019.

“We handled a number of dispositions on behalf of Beneficial and then WSFS,” he said. “We live and breathe this market and have strong existing relationships with likely buyers and lessees, not to mention best-in-class marketing and analytical capabilities.”

Bank branch acquisition opportunities

Equity Retail Brokers frequently connects banking institutions with bank and non-bank businesses (for example, restaurants, Realtors, medical or legal offices, or specialty developers) looking to buy or lease bank real estate. “Banks typically have very good real estate,” Goodman said. “A lot of times, it could be at a corner at a light, or just in a densely populated area on a road with a lot of vehicle traffic. Typically, the better sites garner a lot of interest and lease or sell quickly.”

Drive-thrus are another selling point of many bank branches on the market. “Especially since the onset of Covid, having a drive-thru has become an absolute must for many quick-serve and fast-casual restaurants,” Ginn said.

Seeking to take advantage of this demand for space, some healthy smaller and mid-tier banks have asked Equity Retail Brokers to analyze their portfolios to identify strong candidates for disposition or sale-leaseback or, in the case of leased real estate, to lower occupancy costs by renegotiating with landlords. “Banks can use the liquidity generated by those transactions to help fund their expansion or other strategies, such as building their digital banking platform,” Laiter noted.

In other cases, a smaller bank could work with Equity Retail Brokers to optimize its real estate portfolio and thereby make itself more attractive to prospective merger partners. “If you can demonstrate that you’re running a lean-and-mean portfolio that isn’t going to require a massive overhaul post-merge, that makes you a far-stronger candidate,” Ginn explained.

Conversation is the first step in such productive collaborations—and Equity Retail Brokers can bring an enormous amount of market intelligence to the discussion. “We have data on every single bank branch in our market and their annual deposits,” Goodman explained. “Our in-house analytics capabilities even allow us to provide insights into trends within specific institutions.”

Having closely observed the sector for decades, the team works with a wide variety of bank and non-bank clients. “Once we understand your goals and needs,” Goodman concludes, “we can help you formulate and execute a real estate strategy that gets you where you want to go.”

####